Soil Moisture Sensor Market Size - By Sensors (Volumetric Soil Moisture Sensors and Soil Water Potential Sensors), By Connectivity (Wired and Wireless), By Application (Agriculture, Construction and Mining, Residential, Forestry, Landscaping and Ground Care, Research Studies, Sports, Weather Forecasting others) & Region – Forecasts By 2031

- PUBLISHED ON

- 2024-09-08

- NO OF PAGES

- CATEGORY

- Electronics & Communication

Market Overview:

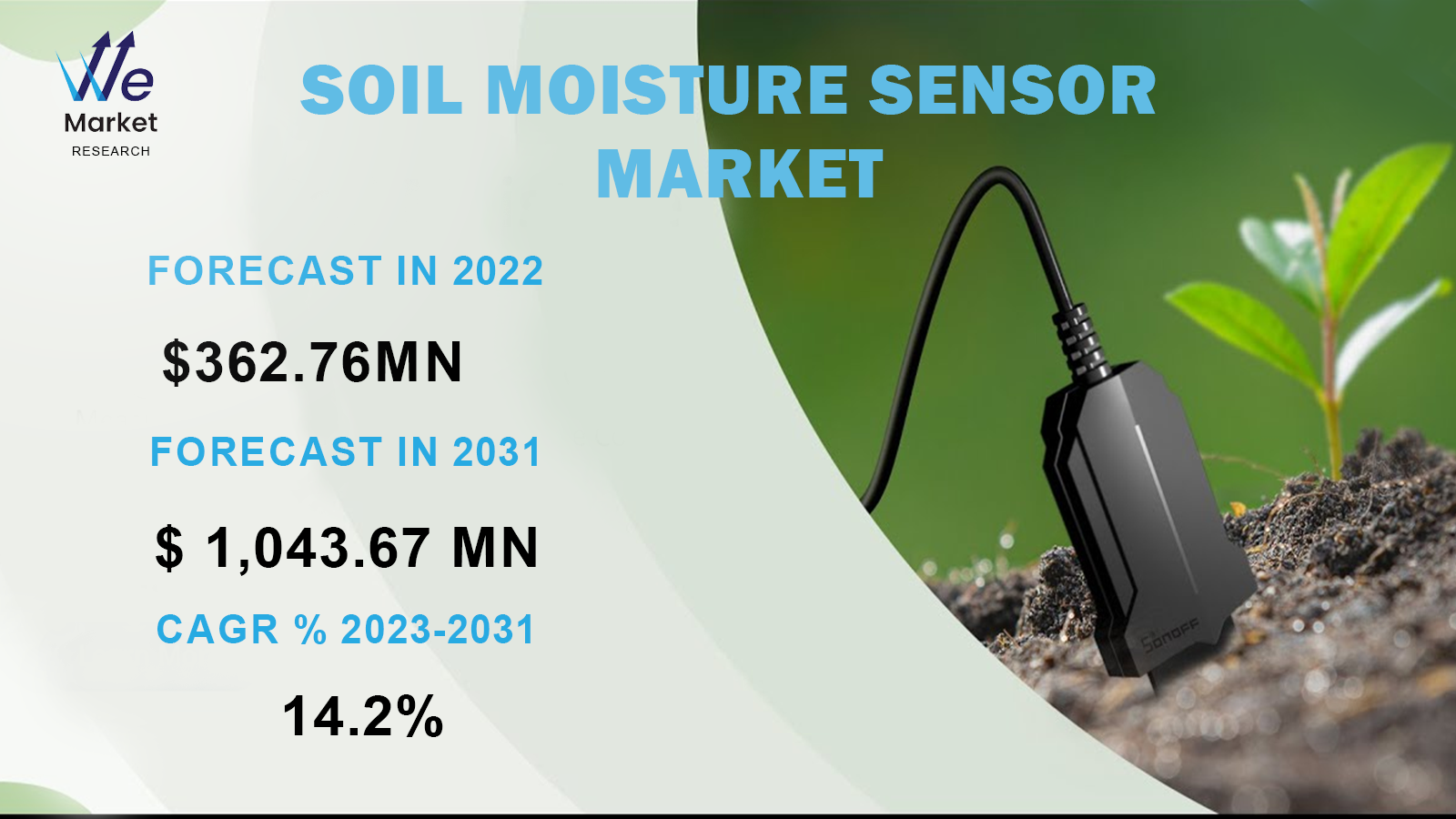

Soil Moisture Sensor Market was valued at USD 362.76 Million in 2022 and expected to grow at a CAGR of 14.2% during the forecast period. A Soil Moisture Sensor is an electronic device designed to measure the moisture content of soil or other growing media. These sensors are commonly used in agriculture, horticulture, environmental monitoring, and research to assess soil moisture levels, optimize irrigation, and make informed decisions about water management.

Soil

moisture sensors operate on various principles, including capacitance,

resistance, and time-domain reflectometry (TDR). Capacitance-based sensors are

the most common and work by measuring changes in electrical capacitance as

moisture content in the soil changes. Resistance-based sensors measure the

electrical resistance between two electrodes in the soil.

Report Scope

|

Report Attributes |

Description |

|

Soil Moisture Sensor Market Size in 2022 |

USD 362.76 Million |

|

Market Forecast in 2031 |

USD 1,043.67 Million |

|

CAGR % 2023-2031 |

14.2% |

|

Base Year |

2022 |

|

Historic Data |

2019-2021 |

|

Forecast Period |

2023-2031 |

|

Report USP |

Production,

Consumption, company share, company heatmap, company production capacity,

growth factors and more |

|

Segments Covered |

Sensors, connectivity, application, region |

|

Regional Scope |

North America,

Europe, APAC, South America and Middle East and Africa |

|

Country Scope |

U.S.; Canada; U.K.; Germany; France; Italy; Spain;

Benelux; Nordic Countries; Russia; China; India; Japan; South Korea;

Australia; Indonesia; Thailand; Mexico; Brazil; Argentina; Saudi Arabia; UAE;

Egypt; South Africa; Nigeria |

|

Key Companies |

Toro Company;

Campbell Scientific Inc.; Spiio; Sentek; METER Group, Inc. USA; Irrometer

Company, Inc.; Acclima Inc.; IMKO Micromodultechnik GmbH; Spectrum Technologies,

Inc.; E.S.I. Environmental Sensors Inc. |

Measurement Range: Soil moisture sensor market can measure

moisture content over a specific range, typically expressed as a percentage.

The range varies depending on the sensor's design and intended application.

Installation: Soil moisture sensors are inserted into

the soil at various depths, depending on the desired measurement depth. Multiple

sensors can be installed at different depths to assess moisture profiles.

Data Output: Soil moisture sensors provide data in

various formats, including analog voltage, digital signals, or through digital

communication protocols such as I2C or UART. Some sensors also offer wireless

data transmission capabilities.

Accuracy and Calibration: Accuracy is a crucial factor in soil

moisture measurements. Sensors may require periodic calibration to ensure

reliable readings, as factors like soil type and temperature can affect their

performance.

Soil

moisture sensor market find applications in agriculture, horticulture,

forestry, and environmental science. Common uses include:

Irrigation management: To optimize water usage by delivering

the right amount of water when and where it's needed.

Crop monitoring: To assess soil moisture conditions for

various crops and prevent over- or under-watering.

Environmental monitoring: To study soil moisture levels in

natural ecosystems, helping to understand climate change impacts and water

availability.

Research: In scientific studies and experiments

that require precise soil moisture data.

Efficient Water

Management: Soil

moisture sensors help conserve water resources by ensuring that irrigation is

applied based on actual soil moisture needs, reducing over-irrigation and water

waste.

Increased Crop Yield: Proper soil moisture management can

improve crop health and yield, as water stress and waterlogging are minimized.

Environmental

Conservation:

Monitoring soil moisture levels in natural habitats can aid in preserving

ecosystems and conserving water resources.

Covid-19 Impact:

The

COVID-19 pandemic had a mixed impact on the Soil Moisture Sensor market, as it

did with many industries. The extent of the impact varied depending on factors

such as regional differences in pandemic severity, the specific application

areas of soil moisture sensors, and the level of reliance on certain

industries. Here's an overview of how the pandemic affected the Soil Moisture

Sensor industry:

Positive Impacts:

Agricultural

Resilience: Agriculture is a major application area for soil moisture sensors,

and the pandemic highlighted the importance of efficient farming practices.

Farmers sought technology solutions, including soil moisture sensors, to

optimize water use and ensure consistent crop yields.

Environmental Monitoring: Environmental monitoring and research

continued during the pandemic, as issues like climate change and water resource

management remained a global priority. Soil moisture sensors played a role in

these efforts, supporting ongoing data collection and analysis.

Research and Development: The pandemic prompted increased

research into sustainable agriculture and environmental science, driving demand

for soil moisture sensors for experimentation and data collection.

Negative Impacts:

Supply Chain Disruptions: The soil moisture sensor market faced

supply chain disruptions, especially in the early stages of the pandemic.

Shutdowns of manufacturing facilities and transportation restrictions affected

the production and distribution of sensors.

Construction and

Landscaping Slowdown:

Some soil moisture sensors are used in construction and landscaping projects to

monitor soil conditions. With lockdowns and economic uncertainty, these sectors

experienced slowdowns, impacting sensor sales.

Delayed Projects: Many agriculture and environmental

projects were delayed or postponed due to pandemic-related uncertainties and

restrictions. This affected the immediate demand for soil moisture sensors.

Economic Downturn: The global economic downturn caused by

the pandemic led to reduced budgets for agriculture, research, and

environmental projects. This, in turn, affected investment in soil moisture

sensors.

Mixed Impacts:

Remote Monitoring and

Automation: The

pandemic accelerated the adoption of remote monitoring and automation

technologies. Soil moisture sensors, when integrated with these technologies,

allowed for remote data collection and management, which was viewed positively

by many industries.

Digital Transformation: Companies and organizations

increasingly recognized the value of digital transformation during the

pandemic. This included the use of sensor data for decision-making, which had a

positive impact on the soil moisture sensor market.

COVID-19

pandemic had both positive and negative effects on the Soil Moisture Sensor

industry. While it highlighted the importance of efficient agriculture and

environmental monitoring, supply chain disruptions, economic challenges, and

delays in projects tempered the immediate market growth. However, as the world

adapts to new norms, the demand for soil moisture sensors is expected to

rebound, especially as industries increasingly prioritize sustainable and

data-driven practices.

Market Dynamics:

Drivers:

Water Scarcity Concerns: Increasing concerns about water

scarcity and the need for efficient water management have driven the adoption

of soil moisture sensors. These sensors help in conserving water resources by

enabling precise irrigation control based on real-time soil moisture data.

Agricultural Efficiency: Agriculture is a major application area

for soil moisture sensors. Farmers use these sensors to optimize irrigation

schedules and improve crop yield and quality. The desire for increased

agricultural productivity and sustainability is a significant driver.

Environmental Monitoring: Soil moisture sensors are essential for

environmental monitoring and research, especially in studying climate change,

soil health, and ecosystem dynamics. Researchers and environmental agencies

rely on these sensors to collect data for analysis and decision-making.

Government Initiatives: Government policies and incentives

promoting sustainable agriculture and water conservation contribute to the

adoption of soil moisture sensors. Incentives may include subsidies for sensor

installation or water-saving practices.

Advancements in Sensor

Technology: Ongoing

advancements in sensor technology have led to the development of more accurate

and reliable soil moisture sensors. These innovations make it easier for

end-users to trust and depend on the data provided by the sensors.

Precision Agriculture: The adoption of precision agriculture

practices, which involve the use of technology for data-driven decision-making,

has led to increased demand for soil moisture sensors. Precision agriculture

aims to optimize resource use and reduce environmental impact.

Smart Farming: Soil moisture sensors are integral to

smart farming systems, where data from sensors can be integrated into digital

platforms for real-time monitoring and control. These systems help farmers make

informed decisions about irrigation, fertilization, and pest control.

Urban Landscaping and

Construction: Soil

moisture sensors are used in landscaping and construction to monitor soil

conditions and ensure proper foundation stability. The growth in urban

development projects has contributed to the demand for these sensors.

Research and Development: Continuous research in agriculture,

environmental science, and soil science drives the need for soil moisture data.

Researchers rely on soil moisture sensors to collect data for experiments,

modeling, and analysis.

Climate Change Mitigation: Soil moisture data is critical for

understanding the impact of climate change on ecosystems and agricultural

practices. As climate change concerns grow, the demand for soil moisture

sensors in climate-related research increases.

Awareness of Sustainable

Practices: Increasing

awareness among farmers, landowners, and environmentalists about the importance

of sustainable land management practices has led to a higher demand for soil

moisture sensors.

Data-Driven

Decision-Making: The

trend toward data-driven decision-making in agriculture and environmental

management has made soil moisture sensors indispensable tools for gathering

critical data for analysis and planning.

Restraints:

Cost

Constraints: Soil moisture sensors can be relatively expensive, especially

high-precision and advanced models. The cost of deploying these sensors across

large agricultural or environmental monitoring areas can be a significant

barrier to adoption, particularly for small-scale farmers and organizations

with limited budgets. Hence, high cost is anticipated to hinder the Soil

Moisture Sensor market demand during the forecast period.

Calibration and

Maintenance: Soil

moisture sensors require periodic calibration to maintain accuracy. Regular

maintenance is also necessary to ensure proper functioning. The need for

technical expertise and the associated costs can be challenging for some users.

Sensor Accuracy and

Variability: The

accuracy of soil moisture sensors can be influenced by various factors,

including soil type, temperature, and sensor placement. Variability in readings

across different soil types and conditions can make data interpretation

challenging.

Installation Complexity: Proper installation of soil moisture

sensors is crucial for obtaining reliable data. Ensuring correct sensor

placement at appropriate depths and locations can be a technical challenge, and

incorrect installation can lead to inaccurate readings.

Sensor Durability: Soil moisture sensors are exposed to

harsh environmental conditions, including moisture, temperature fluctuations,

and physical damage. Ensuring the durability and longevity of sensors in the

field can be a concern.

Compatibility with

Existing Systems:

Integrating soil moisture sensors into existing agricultural or environmental

monitoring systems may require compatibility with specific hardware, software,

or data platforms. Achieving seamless integration can be complex.

Data Interpretation: Accurate data collection is only one

part of the process. Interpreting the data and translating it into actionable

insights can be challenging for end-users, particularly those without a

background in soil science or data analysis.

Education and Awareness: Many potential users may not be aware

of the benefits of soil moisture sensors or may lack the knowledge to use them

effectively. Education and outreach efforts are needed to promote adoption.

Limited Access to Data: In some regions or sectors, access to

soil moisture data may be limited due to data ownership, privacy concerns, or

restrictions on data sharing.

Regulatory and

Certification Challenges:

Compliance with regulatory standards and certification requirements for soil

moisture sensors can add complexity and cost to product development and

deployment.

Environmental Impact: The manufacturing and disposal of

sensors can have environmental implications. Sustainable manufacturing and

recycling practices should be considered.

Market Fragmentation: The Soil Moisture Sensor market is

characterized by a wide range of sensor types, brands, and technologies. This

fragmentation can make it challenging for buyers to select the most suitable

sensor for their specific needs.

Economic Uncertainty: Economic fluctuations and uncertainties

can affect the willingness of farmers, researchers, and organizations to invest

in soil moisture sensors and related technologies. This may hamper the Soil

Moisture Sensor industry during the forecast period.

Regional Analysis:

North America:

United

States: North America, particularly the United States, has a well-established

Soil Moisture Sensor market due to its significant agriculture sector. Farmers

use these sensors to optimize irrigation and improve crop yield. Environmental

monitoring and research also drive sensor adoption.

Canada:

Canada has a growing market for Soil Moisture Sensors, especially in regions

with extensive agricultural activities. The adoption of precision agriculture

practices contributes to sensor demand.

Europe:

Western

Europe: Western European countries like Germany, France, the Netherlands, and

Spain have well-developed agriculture sectors and use Soil Moisture Sensors to

enhance crop management. Environmental monitoring and research also contribute

to sensor adoption.

Nordic

Countries: Nordic countries, including Sweden, Norway, and Finland, have a

strong focus on sustainable agriculture and environmental conservation. These

countries prioritize Soil Moisture Sensors for water-efficient farming

practices.

Asia-Pacific:

China:

China has a rapidly growing agriculture sector, and soil moisture sensor market

play a critical role in optimizing water use and improving crop yield.

Government initiatives to promote efficient farming practices further drive

sensor adoption.

India:

India's agriculture sector relies on monsoon rains, making efficient water

management essential. Soil Moisture Sensors are increasingly used in precision

agriculture to optimize irrigation.

Australia:

Australia faces challenges related to water scarcity and droughts. Soil Moisture

Sensors are crucial for managing limited water resources effectively.

Latin America:

Brazil:

Brazil's large agriculture sector, including sugarcane, soybeans, and coffee,

drives demand for Soil Moisture Sensors. Precision agriculture practices are

becoming more common.

Argentina:

Argentina's agriculture industry benefits from sensor adoption, particularly in

regions with varying climate conditions.

Middle East and Africa:

In

regions of the Middle East and North Africa (MENA) with agriculture, Soil Moisture

Sensors help address water scarcity challenges. Israel, in particular, has a

well-developed market for efficient irrigation technologies.

In

parts of Sub-Saharan Africa, Soil Moisture Sensors support small-scale

agriculture and aid in mitigating the impact of climate change on food

security.

Oceania:

Australia

and New Zealand have strong agriculture sectors, and Soil Moisture Sensors are

used to manage water resources efficiently, especially in the face of drought

conditions.

Competitive Landscape:

The

global Soil Moisture Sensor market is highly competitive and fragmented with

the presence of several players. These companies are constantly focusing on new

product development, partnerships, collaborations, and mergers and acquisitions

to maintain their market position and expand their geographical presence.

Some of the key players

operating in the Soil Moisture Sensor market are:

·

Toro

Company

·

Campbell

Scientific Inc.

·

Spiio

·

Sentek

·

METER

Group, Inc. USA

·

Irrometer

Company, Inc.

·

Acclima

Inc.

·

IMKO

Micromodultechnik GmbH

·

Spectrum

Technologies, Inc.

·

E.S.I.

Environmental Sensors Inc.

·

Others

Segments for Soil Moisture Sensor Market

By Sensors

·

Volumetric Soil Moisture Sensors

o Capacitance

o Probes

o Time Domain Transmissometry (TDT)

·

Soil Water Potential Sensors

o Gypsum Blocks

o Tensiometers

o Granular Matrix

By Connectivity

·

Wired

·

Wireless

By Application

·

Agriculture

·

Construction and Mining

·

Residential

·

Forestry

·

Landscaping and Ground Care

·

Research Studies

·

Sports

·

Weather Forecasting

·

Others

By Geography

·

North

America

o

U.S.

o

Canada

o

Mexico

·

Europe

o

U.K.

o

Germany

o

France

o

Italy

o

Spain

o

Russia

·

Asia-Pacific

o

Japan

o

China

o

India

o

Australia

o

South

Korea

o

ASEAN

o

Rest

of APAC

·

South

America

o

Brazil

o

Argentina

o

Colombia

o

Rest

of South America

·

MEA

o

South

Africa

o

Saudi

Arabia

o

UAE

o

Egypt

o

Rest

of MEA

1. Global

Soil Moisture Sensor Market Introduction and Market Overview

1.1. Objectives

of the Study

1.2. Soil Moisture Sensor Market

Definition & Description

1.3. Global

Soil Moisture Sensor Market Scope and Market Estimation

1.3.1.

Global Soil Moisture Sensor Overall

Market Size, Revenue (US$ Mn), Market CAGR (%), Market forecast (2023 - 2033)

1.3.2.

Global Soil Moisture Sensor

Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2019 - 2033

1.4. Market

Segmentation

1.4.1.

Sensors of Global Soil Moisture

Sensor Market

1.4.2.

Connectivity of Global Soil

Moisture Sensor Market

1.4.3.

Application of Global Soil

Moisture Sensor Market

1.4.4.

Region of Global Soil Moisture

Sensor Market

2. Executive Summary

2.1. Global

Soil Moisture Sensor Market

Industry Trends under COVID-19 Outbreak

2.1.1.

Global COVID-19 Status Overview

2.1.2.

Influence of COVID-19 Outbreak on

Global Soil Moisture Sensor Market

Industry Development

2.2. Market

Dynamics

2.2.1.

Drivers

2.2.2.

Limitations

2.2.3.

Opportunities

2.2.4.

Impact Analysis of Drivers and

Restraints

2.3. Pricing

Trends Analysis & Average Selling Prices (ASPs)

2.4. Key

Mergers & Acquisitions, Expansions, JVs, Funding / VCs, etc.

2.5. Porter’s

Five Forces Analysis

2.5.1.

Bargaining Power of Suppliers

2.5.2.

Bargaining Power of Buyers

2.5.3.

Threat of Substitutes

2.5.4.

Threat of New Entrants

2.5.5.

Competitive Rivalry

2.6. Value

Chain / Ecosystem Analysis

2.7. PEST

Analysis

2.8. Russia-Ukraine

War Impacts Analysis

2.9. Economic

Downturn Analysis

2.10.

Market Investment Opportunity

Analysis (Top Investment Pockets), By Segments & By Region

3. Global Soil Moisture Sensor

Market

Estimates & Historical Trend Analysis (2020 - 2022)

4. Global Soil Moisture Sensor

Market

Estimates & Forecast Trend Analysis, by Sensors

4.1. Global

Soil Moisture Sensor Market Revenue (US$ Mn) Estimates and Forecasts, by Sensors,

2022 to 2033

4.1.1.1.

Volumetric Soil Moisture Sensors

4.1.1.1.1.

Capacitance

4.1.1.1.2.

Probes

4.1.1.1.3.

Time Domain Transmissometry (TDT)

4.1.1.2.

Soil Water Potential Sensors

4.1.1.2.1.

Gypsum Blocks

4.1.1.2.2.

Tensiometers

4.1.1.2.3.

Granular Matrix

5. Global Soil Moisture Sensor

Market

Estimates & Forecast Trend Analysis, by Connectivity

5.1. Global

Soil Moisture Sensor Market Revenue (US$ Mn) Estimates and Forecasts, by Connectivity,

2022 to 2033

5.1.1.

Wired

5.1.2.

Wireless

6. Global Soil Moisture Sensor

Market

Estimates & Forecast Trend Analysis, by Application

6.1. Global

Soil Moisture Sensor Market Revenue (US$ Mn) Estimates and Forecasts, by Application,

2022 to 2033

6.1.1.

Agriculture

6.1.2.

Construction and Mining

6.1.3.

Residential

6.1.4.

Forestry

6.1.5.

Landscaping and Ground Care

6.1.6.

Research Studies

6.1.7.

Sports

6.1.8.

Weather Forecasting

6.1.9.

Others

7. Global Soil Moisture Sensor

Market

Estimates & Forecast Trend Analysis, by Region

7.1. Global

Soil Moisture Sensor Market Revenue (US$ Mn) Estimates and Forecasts, by Region,

2022 to 2033

We Market Research senior executive is assigned to each consulting engagement and works closely with the project team to deliver as per the clients expectations. Market Research Process We Market Research monitors 3 important attributes during the QA process- Cost, Schedule & Quality. We believe them as a critical benchmark in achieving a project’s success. One of the key manufacturers of automotive had plans to invest in electric utility vehicles. The electric cars and associated markets being a of evolving nature, the automotive client approached We Market Research for a detailed insight on the market forecasts. The client specifically asked for competitive analysis, regulatory framework, regional prospects studied under the influence of drivers, challenges, opportunities, and pricing in terms of revenue and sales (million units). The overall study was executed in three stages, intending to help the client meet its objective of precisely understanding the entire market before deciding on an investment. At first, secondary research was conducted considering political, economic, social, and technological parameters to get a gist of the various aspects of the market. This stage of the study concluded with the derivation of drivers, opportunities, and challenges. It also laid substantial emphasis on understanding and collecting data not only on a global scale but also on the regional and country levels. Data Extraction through Primary Research The second stage involved primary research in which several market players and automotive parts suppliers were contacted to study their viewpoint concerning the development of their market and production capacity, clientele, and product line. This stage concluded in a brief understanding of the competitive ecosystem and also glanced through the strategies and pricing of the companies profiled. In the final stage of the study, market forecasts for the electric utility were derived using multiple market engineering approaches. This data helped the client to get an overview of the market and accelerate the process of investment. Business process outsourcing, being one of the lucrative markets from both supply- and demand- side, has appealed to various companies. One of the prominent corporations based out of Japan approached us with their requirements regarding the scope of the procurement outsourcing market for around 50 countries. Additionally, the client also sought key players operating in the market and their revenue breakdown in terms of region and application. Business Solution An exhaustive market study was conducted based on primary and secondary research that involved factors such as labor costs in various countries, skilled and technical labors, manufacturing scenario, and their respective contributions in the global GDP. A comparative study of the market was conducted from both supply- and demand side, with the supply-side comprising of notable companies, such as GEP, Accenture, and others, that provide these services. On the other hand, large manufacturing companies from them demand-side were considered that opt for these services. Conclusion The report aided the client in understanding the market trends, including country-level business scenarios, consumer behavior, and trends in 50 countries. The report also provided financial insights of crucial players and detailed market estimations and forecasts till 2033.Quality Assurance Process

To mitigate risks that can impact project success, we deploy the follow project delivery best practices:

Case Study- Automotive Sector

Solution

Market Estimates and Forecast

Case Study- ICT Sector

}})

Select a license type that suits your business needs

US $3499

Only Three Thousand Four Hundred Ninety Nine US dollar

- 1 User access

- 15% Additional Free Customization

- Free Unlimited post-sale support

- 100% Service Guarantee until achievement of ROI

US $4499

Only Four Thousand Four Hundred Ninety Nine US dollar

- 5 Users access

- 25% Additional Free Customization

- Access Report summaries for Free

- Guaranteed service

- Dedicated Account Manager

- Discount of 20% on next purchase

- Get personalized market brief from Lead Author

- Printing of Report permitted

- Discount of 20% on next purchase

- 100% Service Guarantee until achievement of ROI

US $5499

Only Five Thousand Four Hundred Ninety Nine US dollar

- Unlimited User Access

- 30% Additional Free Customization

- Exclusive Previews to latest or upcoming reports

- Discount of 30% on next purchase

- 100% Service Guarantee until achievement of ROI